What does negative income tax mean on income statement?

Negative income tax is a system where cash is given by the government to eligible tax residents who are earning below a certain threshold.

Which of the following expenses is not paid in cash?

From the above mentioned expenses, Depreciation is the expense which is not paid in Cash. ↬ Depreciation refers to a permanent, gradual and continuous decrease in the value of a fixed asset and it continues till the end of the useful life of the asset. It is a charge against profit.

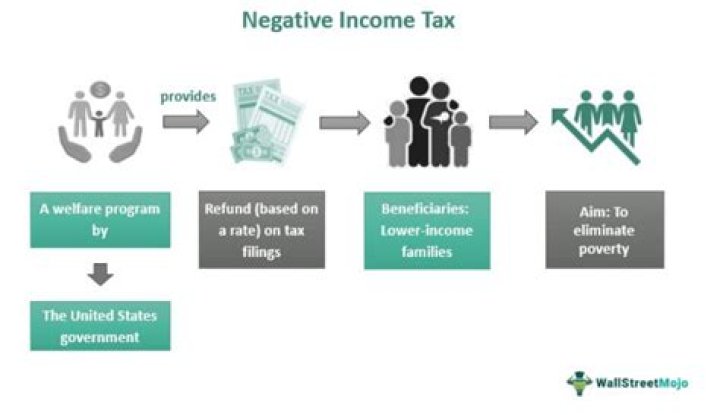

What is negative income tax? The negative income tax is a way to provide people below a certain income level with money. In contrast to a standard income tax, where people pay money to the government, people with low incomes would receive money back from the government.

Do you pay taxes if your income is negative?

If you have a negative taxable income, it is counted as a zero taxable income. The IRS does not provide an income tax refund amount for having a negative taxable income. Having a negative taxable income is not bad; it simply means that you have no tax liability.

What should I claim as a tax deduction for 2010?

The experts say she should only deduct enough to get to the start of her current tax bracket. In this case, she should claim only $9,000 for 2010. That would reduce her income for tax purposes from $50,000 to $41,000, where the 31.2 per cent marginal tax bracket starts.

Is it possible to have negative net income?

Net income is commonly referred to as the bottom line since it sits at the bottom of the income statement. Yes, there are times when a company can have positive cash flow while reporting negative …

Is it worth it to defer income tax for a year?

But if you expect to earn $60,000 in 2011, you will be paying tax at a 31 per cent marginal rate. So that $3,000 deduction would be worth $935 if you deferred it by a year. That’s an extra $215 in your pocket just for delaying the deduction for a year.

When does it pay to defer tax claims and deductions?

So tax specialists say if you don’t crack the $200 limit one year, it could benefit you to delay making that claim. A $200 claim in each of two years would yield a tax credit of $30 each year, for a total of $60. But a $400 claim in one year would yield a federal tax credit of $30 for the first $200 and $58 for the second $200, for a total of $88.