What happens if I have two Roth IRAs?

Having multiple Roth IRA accounts is perfectly legal, but the total contribution you put into both accounts still cannot exceed the federally set annual contribution limits.

Can you have 2 ROTH IRAs accounts?

How many Roth IRAs? There is no limit on the number of IRAs you can have. You can even own multiples of the same kind of IRA, meaning you can have multiple Roth IRAs, SEP IRAs and traditional IRAs. That said, increasing your number of IRAs doesn’t necessarily increase the amount you can contribute annually.

When were Roth IRA first available?

1997

The Roth IRA was introduced as part of the Taxpayer Relief Act of 1997 and is named for Senator William Roth.

Can you have 2 Roth IRAs accounts?

What year did the Roth IRA start?

What does the 5 year rule mean for Roth IRA?

The 5-year rule essentially states that five tax years must pass from when the first contribution is made to (any) Roth IRA, until a qualified distribution can be made. Because the measurement is based on tax years, this means that a contribution (not just a rollover, but an actual new contribution)…

How are withdrawals from a Roth IRA taxed?

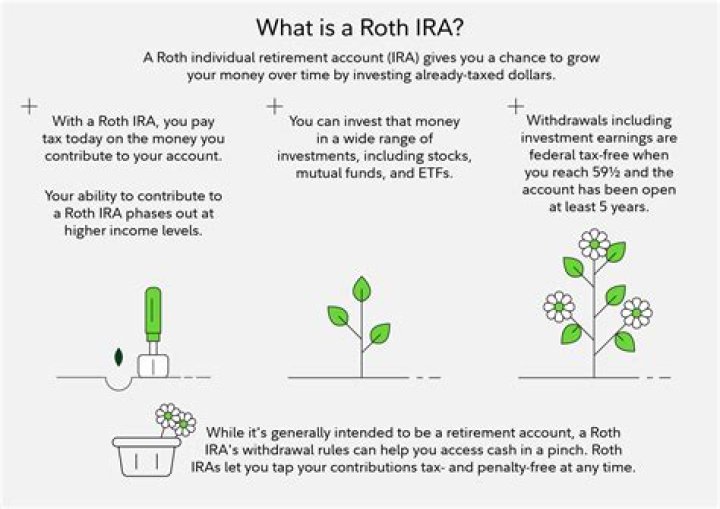

How Roth IRA Withdrawals Are Taxed. You can withdraw contributions at any time, for any reason, with no tax or penalty. You’ve already paid taxes, and the IRS considers it your money. You can always withdraw your Roth IRA contributions without owing taxes or penalties. Withdrawals of earnings work differently.

What kind of taxes do you pay on a Roth IRA?

If you take a non-qualified distribution from your Roth IRA, the earnings portion will be included in your modified adjusted gross income (MAGI) to determine Roth IRA eligibility. 13 3 Tax and 10% penalty on earnings. You may be able to avoid both if you have a qualified exception Tax and 10% penalty on earnings.

When do I have to contribute to a Roth IRA?

Roth IRAs offer tax-free growth on both the contributions and the earnings that accrue over the years. If you play by the rules, you won’t pay taxes when you take the money out. 1 In 2020 and 2021, the contribution limits are set at $6,000, and an additional $1,000 may be contributed by those who are age 50 or older. 2