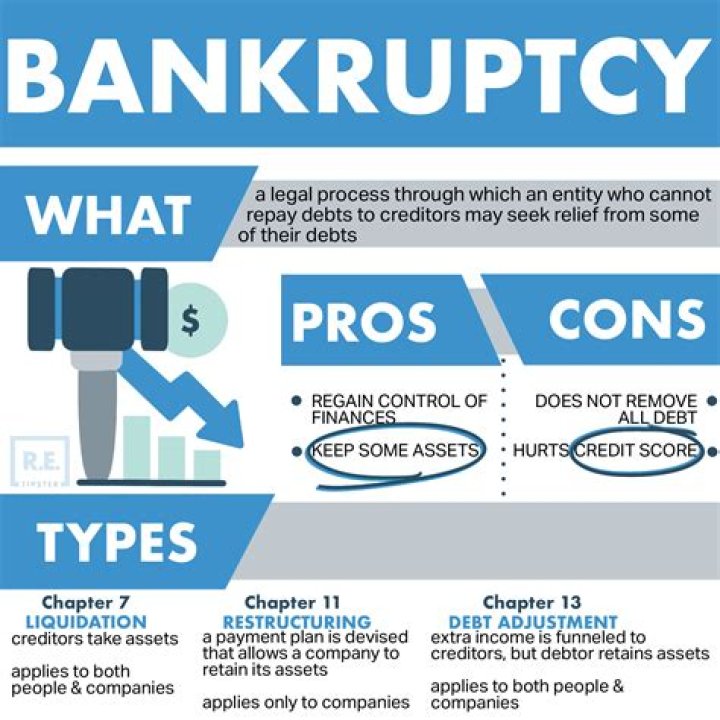

What happens to my properties when I go bankrupt?

When you become bankrupt, your trustee[?] becomes the owner of your share of any house or property that you own. This means your trustee now has control over the property and can sell it to help pay your debts.

Would you lose your house if you went bankrupt?

If you rent your home, it’s unlikely you’ll lose it by going bankrupt. However, there are certain situations where your home may be at risk, including: if the property is included in the bankruptcy estate – although this won’t apply to most regulated, secure and assured tenancies.

Can I declare myself bankrupt and keep my house?

You’ll usually be able to stay in your home after bankruptcy if your rent payments are up to date. If you have rent arrears, this debt will be included in your bankruptcy. Your landlord can’t take any court action to get this money back from you, but they can still evict you.

Can HMRC take my house?

They can only take property owned by the company – no hired or rented means, nor property under your own name. If your company fails to pay its debts with HMRC, they will perform enforcement actions, to get the money they are owed.

How do you rent when bankrupt?

You can apply to rent a home from a private landlord during or after bankruptcy. However before accepting you as a tenant, the landlord might check the Insolvency Register or credit file. This could mean you find it hard to rent a home, or you could be asked for a guarantor or larger deposit.

Can HMRC send bailiffs?

If you do not pay, HMRC can ask the court to: send bailiffs to take and sell things that you own to cover the debt. take the money directly from your earnings. make you bankrupt or close down your company.

Does going bankrupt affect renting?

Bankruptcy only covers the debts that you owed before you became bankrupt, not after. So, just like every other tenant, you’ll still be liable for the rental fees you incur after the date of your bankruptcy.

Can you bankrupt and keep your house?

It’s possible to keep a home when you file for bankruptcy, but the circumstances must be right. For instance, Chapter 7 filers must be current on payments and protect all home equity with a bankruptcy exemption. By contrast, Chapter 13 filers can catch up on missed mortgage payments and keep the home.