What happens to your Thrift Savings Plan if you die?

The death benefit payment will be made directly to the beneficiary or to an “inherited” IRA. If a beneficiary participant dies, the new beneficiary(ies) cannot continue to maintain the account in the TSP. Also, the death benefit payment can- not be transferred or rolled over into any type of IRA or plan.

What happens if nominated beneficiary dies?

It is only on the policy owner’s death that the nominated beneficiary is entitled to accept the benefit and the insurer is obligated to pay the proceeds of the policy to the beneficiary. Put simply, when the nominated beneficiary dies, the ‘expectation’ evaporates. It falls away.

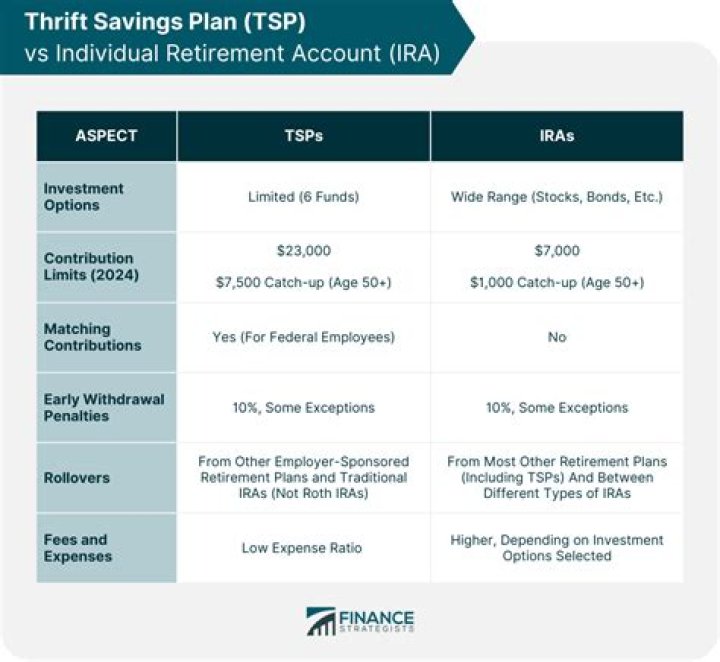

Is Thrift Saving Plan a pension?

If you’re covered by the Federal Employees’ Retirement System (FERS), the TSP is one part of a three-part retirement package that also includes your FERS basic annuity and Social Security.

Can a qualified plan beneficiary pass outside the estate?

Beneficiary Designation and the Estate. Generally, qualified plan assets pass outside the estate. The qualified plan beneficiary designation form, not the will, names who is to receive the retirement plan assets.

How are death benefits paid to the beneficiary?

Death benefit payments made from your beneficiary participant account must be paid directly to your beneficiary (ies). These payments cannot be transferred or rolled over into an IRA or eligible employer plan. In addition, the payment will be fully taxable in the year your beneficiary (ies) receive it.

Who are the beneficiaries of a health savings account?

Health Savings Accounts: Death of an account owner 1 Overview. A Health Savings Account (HSA) owner may designate any person or nonindividual, including his/her estate, as the death beneficiary of his/her HSA. 2 Spouse beneficiary. 3 Nonspouse beneficiary. 4 Estate as beneficiary. 5 IRS reporting after death. 6 Conclusion. …

When do you need a qualified plan beneficiary designation?

The qualified plan beneficiary designation form, not the will, names who is to receive the retirement plan assets. The designation could be to the estate, but then the will would likely have to be used to pay out the retirement plan, which generally requires probate first. A qualified plan may require one year of marriage before QJSA rules apply.