What is a 401k lump-sum distribution?

A lump-sum distribution is a financial term that usually refers to an election to receive a 401(k) plan or pension benefit as a one-time payment for the entire balance. Instead of taking the payments throughout retirement, you can cash out the entire policy at once.

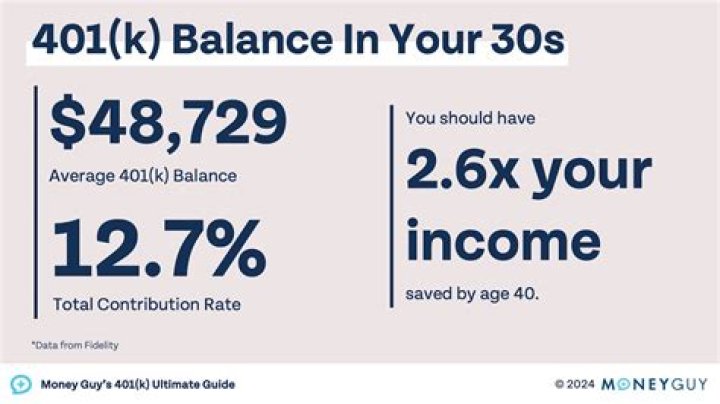

What is a good 401K balance at age 40?

By 40, Fidelity recommends having three times your salary put away. If you earn $50,000 a year, you should aim to have $150,000 in retirement savings by the time you are 40. If your annual salary is $100,000 a year, you should aim to have $300,000 saved.

What is an NUA distribution?

NUA relates to distributions of appreciated employer securities from an eligible employer-based retirement plan. Taxation of NUA following a lump-sum distribution is deferred until the securities are sold or disposed of. When securities are sold, any NUA is taxed at the long-term capital gains rate.

When to take a lump sum from your 401k?

Options When You Leave an Employer. Lump-sum withdrawal options are not as limited when you leave an employer for another job or if you retire. You can take a lump-sum distribution from a previous employer’s 401(k) plan up to the total vested account balance.

Why is Nua important for 401k retirement plan?

The NUA is important if you are distributing highly appreciated company stock from your tax-deferred employer-sponsored retirement plan, such as a 401 (k).

When do you have to make a Nua distribution?

However, none of the money can stay in the plan past the end of that year. 3) The lump-sum distribution must be made after a “triggering event”. In order to be eligible for NUA treatment of an in-kind distribution of employer stock, the lump-sum distribution must be made after a triggering event.

When do you have to make a lump sum distribution?

No partial distributions are permitted – the lump sum distribution must take place within one year of a) separation from your employer, b) reaching the minimum age for distribution, c) becoming disabled, or d) being deceased. The distribution must include all assets from all accounts sponsored by and held through the same employer