What is a lump-sum cash distribution?

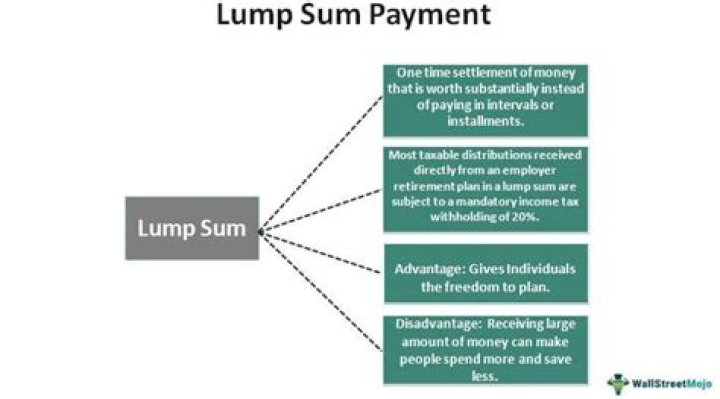

A lump-sum distribution is an amount of money due that is paid all at once, as opposed to being paid in regular installments. Lump-sum distributions may be made from retirement plans, commissions earned, windfall earnings, or certain fixed-income investments.

What can I do with a lump-sum pension distribution?

A lump sum amount can be rolled over to an Individual Retirement Account (IRA) and avoid taxation when you receive the lump sum. However, any distributions from the IRA will be taxed as ordinary income. If the money isn’t rolled over, you’ll pay ordinary income tax on the amount of the lump sum.

What is a lump-sum relocation package?

If you’re not familiar with the concept, a lump sum relocation typically consists of a single, fixed amount provided to an employee by an employer to move to a destination. Global mobility professionals often view this as a simple way to get employees into a new role quickly.

When is a lump sum payment considered a distribution?

A lump-sum distribution is a distribution of the entire balance of a qualified retirement plan within one tax year. Thus, a series of payments received within one tax year will be considered a lump-sum distribution if the entire balance of a particular type of retirement plan, such as a profit sharing, pension,…

Do you have to consent to a lump sum distribution?

However, married taxpayers must obtain the consent of the spouse to elect a lump-sum distribution. A lump-sum distribution is a distribution of the entire balance of a qualified retirement plan within one tax year.

What kind of income is reported as a lump sum?

Lump-Sum Distributions. A taxable lump-sum distribution is reported as ordinary pension income on Form 1099-R, Distributions from Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc., unless the taxpayer was born before January 2, 1936, in which case, a special averaging procedure can be used.

How can I avoid taxes on a lump sum distribution?

A tax on a lump-sum distribution can be avoided if it is rolled over to another retirement account within 60 days of receiving it. However, the plan administrator is required to withhold 20% of the distribution for the payment of taxes. The 20% withholding can be avoided if the rollover is done as a direct transfer, from trustee to trustee.