What is a short term tax return?

A short tax year is a tax year of less than 12 months. A short period tax return may be required when you (as a taxable entity): Are not in existence for an entire tax year, or. Change your accounting period.

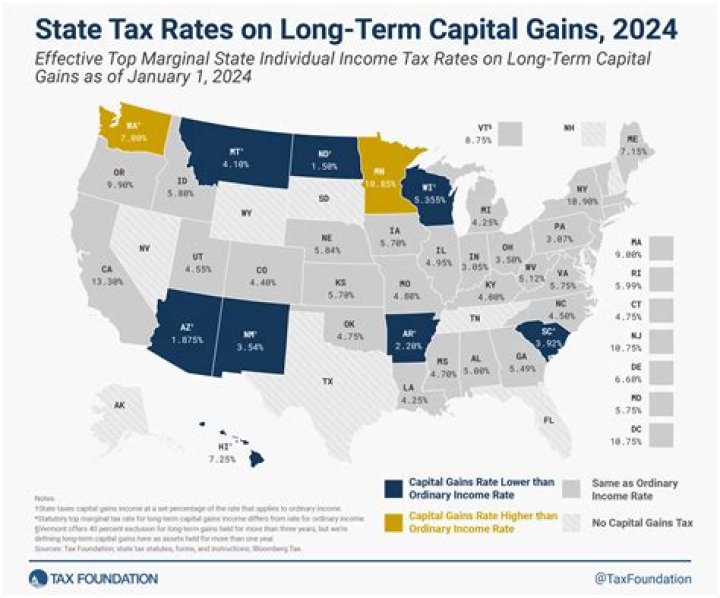

Do you have to pay taxes on short term?

Any income you receive from investments that you held for less than a year must be included in your taxable income for that year.2 For example, if you have $80,000 in taxable income from your salary and $10,000 from short-term investments, then your total taxable income is $90,000.

Who should fill schedule 112A?

The ITR forms contain schedule 112A to fill scrip wise details of these listed securities sold during a financial year. A taxpayer having long-term capital gains under the grandfathering provisions of section 112A should mandatorily fill the details in schedule 112A.

When to use a short form tax return?

Short Form Tax Returns You can use the 1040-EZ form if you file as single or married filing jointly and with no dependents. Total income for you and a spouse must be under $100,000 with less than $1,500 in interest income. Don’t use 1040-EZ if you have to report self-employment income or capital gains or losses.

When to use the 1040 Long Form tax form?

You can claim more tax breaks when you use the 1040 long form. You can use the 1040-EZ form if you file as single or married filing jointly and with no dependents. Total income for you and a spouse must be under $100,000 with less than $1,500 in interest income.

Can You claim tax breaks on a short form?

First, not everyone can use a short form. Second, the tax breaks you can claim on short forms are limited. You can claim more tax breaks when you use the 1040 long form. You can use the 1040-EZ form if you file as single or married filing jointly and with no dependents.

What are the tax exceptions for surviving spouse?

Surviving spouse. Surrender of policy for cash. Terminally or chronically ill defined. Exception. Main home. Repaying the first-time homebuyer credit. Joint returns. Reduced exclusion. Expatriation tax. Exception to use test for individuals with a disability.