What is ABC in manufacturing?

Activity-based costing (ABC) is mostly used in the manufacturing industry since it enhances the reliability of cost data, hence producing nearly true costs and better classifying the costs incurred by the company during its production process.

How do you find the unit product cost using ABC?

To calculate the per unit overhead costs under ABC, the costs assigned to each product are divided by the number of units produced. In this case, the unit cost for a hollow center ball is $0.52 and the unit cost for a solid center ball is $0.44.

What are the steps of calculating the Activity Based Costing?

Step 1: Identify the products that are the chosen cost objects. Step 2: Identify the direct costs of the products Step 2: Identify the direct costs of the products. Step 3: Select the activities and cost-allocation bases to use for allocating indirect costs to the products for allocating indirect costs to the products.

Which of the following is a limitation of ABC costing?

Disadvantages of ABC: It is impossible to allocate all overhead costs to specific activities. The choice of both activities and cost drivers might be inappropriate. ABC can be more complex to explain to the stakeholders of the costing exercise. The benefits obtained from ABC might not justify the costs.

What is the ABC to do list?

The ABC Method was originally developed by Alan Lakein and consists of assigning a priority status of “A,” “B,” or “C” to each of the items of your to-do list or task list. High priority, very important, critical items, with close deadlines or high level importance to them.

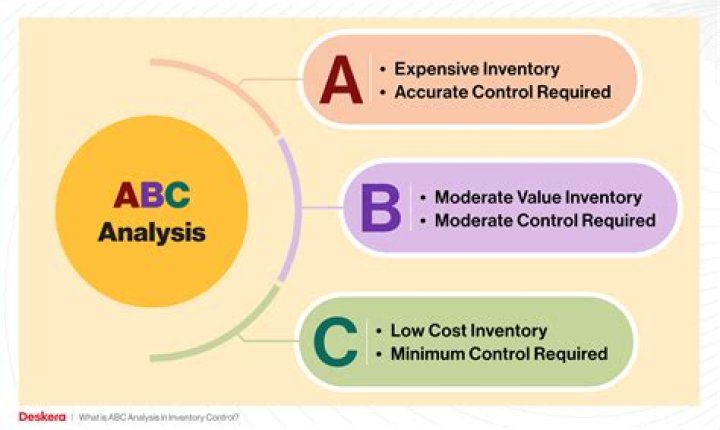

What is the goal of ABC?

The goal of ABC classification is to provide a way for a business to identify that valuable 20% so that segment can be controlled most closely. Once the A’s, B’s and C’s have been identified, each category can be handled in a different way, with more attention being devoted to category A, less to B, and even less to C.

How are ABC product costs determined?

(Figure)How are costs allocated in an ABC system? Estimated overhead costs are first allocated to activity cost pools. Then, an allocation rate is determined based on the estimated usage of the cost driver for that pool. Then the costs are allocated to each product based on that product’s cost driver usage.

How do you calculate overhead using Activity-Based Costing?

The five steps are as follows:

- Identify costly activities required to complete products.

- Assign overhead costs to the activities identified in step 1.

- Identify the cost driver for each activity.

- Calculate a predetermined overhead rate for each activity.

- Allocate overhead costs to products.

What are the limitations of ABC system?

Disadvantages of ABC: ABC will be of limited benefit if the overhead costs are primarily volume related or if the overhead is a small proportion of the overall cost. It is impossible to allocate all overhead costs to specific activities. The choice of both activities and cost drivers might be inappropriate.

When do you use ABC in product costing?

ABC has been accepted as very useful for product costing where production overheads are high in relation to direct cost, where there is diversity in the product range, where products consume different amount of overhead and where consumption of overhead is not basically driven by their volume. 1.

What are the strengths of ABC manufacturing company?

In the strengths, management should identify the following points exists in the organization: Activities of the company better than competitors. Unique resources and low cost resources company have. Activities and resources market sees as the company’s strength. Unique selling proposition of the company. Improvement that could be done.

How long should introduction be for ABC manufacturing company?

The challenging diagnosis for Abc Manufacturing Company and the management of information is needed to be provided. However, introduction should not be longer than 6-7 lines in a paragraph. As the most important objective is to convey the most important message for to the reader. After introduction, problem statement is defined.

What can be avoided for ABC manufacturing company?

Activities that can be avoided for Abc Manufacturing Company. Activities that can be determined as your weakness in the market. Factors that can reduce the sales. Competitor’s activities that can be seen as your weakness. Good opportunities that can be spotted. Interesting trends of industry. Changes in social patterns and lifestyles.