What is income or loss?

Income loss means an amount equal to the loss of income incurred by an injured person usually engaged in a remunerative occupation, within one year after the date of the accident, and as a result of disability caused by the accident.

What is total income loss?

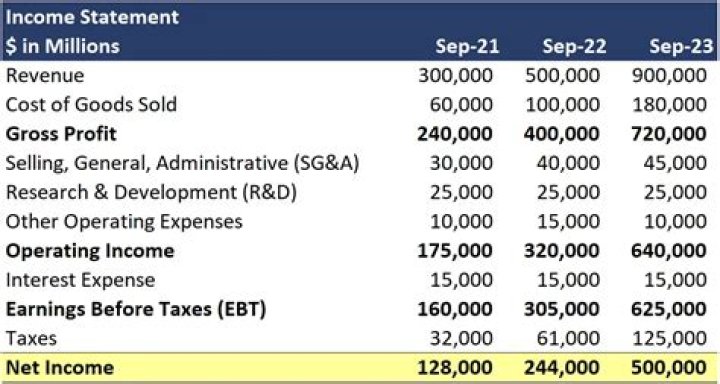

Net income or loss is what remains after subtracting all expenses from revenue. A net loss results when total expenses exceed total revenue for an accounting period, such as a month or a year. A sustained period of losses leads to dwindling cash reserves, which could mean bankruptcy.

How do you calculate loss income?

Take the amount of your hourly wage and multiply it by the number of hours you missed due to the accident. For example, if your hourly wage is $20, and you missed work for three days (8 hours per day), your calculation would be: $20 x (8 hrs x 3 days) = $480 (your total lost wages).

What does it mean when it says net income loss?

A net loss is when expenses exceed the income or total revenue produced for a given period of time. It is sometimes called a net operating loss (NOL). Businesses that have a net loss don’t necessarily go bankrupt because they may opt to use their retained earnings or loans to stay afloat.

Is a net income loss bad?

A net loss will cause a decrease in retained earnings and stockholders’ equity. A sole proprietorship’s net income will cause an increase in the owner’s capital account, which is part of owner’s equity. A net loss will cause a decrease in the owner’s capital account and owner’s equity.

How do you determine a company’s income limit?

Subtract your business’s expenses and operating costs from your total revenue. This calculates your business’s earnings before tax. Deduct taxes from this amount to find you business’s net income. Your net income will be your business income.

How do you calculate income from business or profession?

How is income from business or profession computed?

- Expenditure incurred during the previous year wholly and exclusively for the purpose of the business;

- After deducting allowances and deductions provided in Sections 30 to 43D of the I.T. Act. 1961;

- The following expenses are not alloweable:-