What is meant by tax buoyancy?

Tax buoyancy is an indicator to measure efficiency and responsiveness of revenue mobilization in response to growth in the Gross domestic product or National income. A tax is said to be buoyant if the tax revenues increase more than proportionately in response to a rise in national income or output.

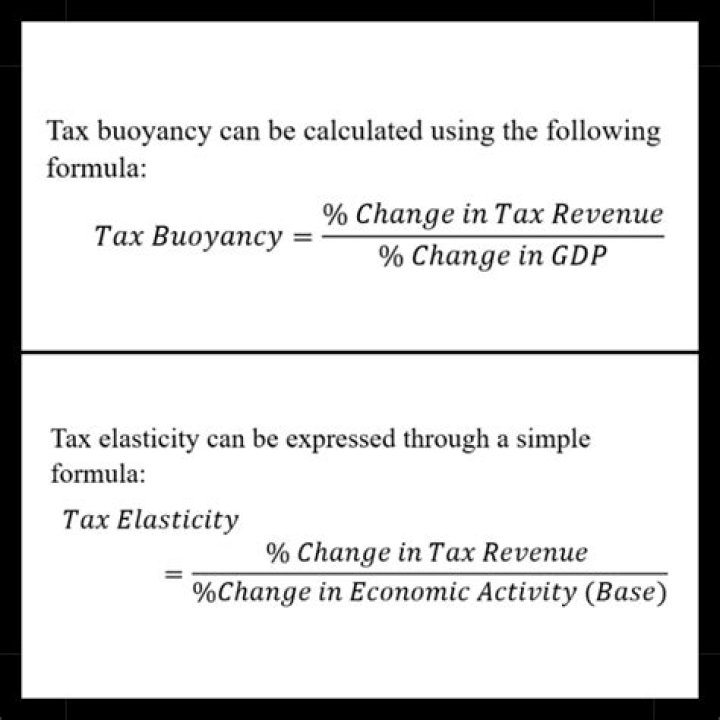

How is tax buoyancy calculated?

Tax buoyancy is an important indicator of the efficiency and responsiveness of tax revenue mobilisation to GDP growth. It is calculated as a ratio of percentage growth in tax revenues to growth in nominal GDP for a given year.

What is a good tax buoyancy?

A tax buoyancy coefficient equal to 1 implies that tax revenue grows at the same pace as the economy/base whereas a tax buoyancy below 1 insinuates that tax revenue grows at a slower pace than the economy/base. The total tax revenue buoyancy estimate is 0.82 both in the short-run and long-run.

What is tax buoyancy Upsc?

Tax buoyancy explains relationship between the changes in government’s tax revenue growth and the changes in GDP. It refers to the responsiveness of tax revenue growth to changes in GDP. When a tax is buoyant, its revenue increases without increasing the tax rate. A similar looking concept is tax elasticity.

Can tax buoyancy be negative?

Tax buoyancy is one of the key indicators to assess the efficiency of a government’s tax system. It measures the responsiveness of tax mobilisation to economic growth. Thus, tax buoyancy was in negative territory, the only time it has been so low in the post-reforms era.

What is buoyancy in economy?

Buoyant is a term used to describe a commodities or equity market where the prices are generally rising and when there are considerable signals of strength. These markets have similar features to bull markets, although a buoyant market may not necessarily last as long.

What are the features of buoyant economy?

Buoyant markets usually display characteristics of high corporate profits, low cost of capital and a high return on capital. Markets that are considered to be buoyant have strong underlying performance, specifically higher-than-average corporate price-to-earnings ratios (P/E ratio) and profit margins.

What is the meaning of buoyant economy?

adjective. A buoyant economy is a successful one in which there is a lot of trade and economic activity. We have a buoyant economy and unemployment is considerably lower than the regional average. High interest rates do not point to a buoyant market this year. Analysts expect the share price to remain buoyant.

The total tax revenue buoyancy estimate is 0.82 both in the short-run and long-run. This is almost in line with the National Treasury value of 0.91 (National Treasury, 2017). Also, this implies that the growth in tax revenue did not match the growth of the economy in South Africa over the estimation period.

It is calculated as a ratio of percentage growth in tax revenues to growth in nominal GDP for a given year. Tax is said to be buoyant if the gross tax revenues increase more than proportionately in response to a rise in GDP figures.

What Is Buoyant? Buoyant is a term used to describe a commodities or equity market where the prices are generally rising and when there are considerable signals of strength. These markets have similar features to bull markets, although a buoyant market may not necessarily last as long.

Which is the best definition of Tax buoyancy?

The concepts of tax buoyancy or tax efficiency are used to measure the responsiveness of tax revenue to the economic growth. Tax buoyancy is a crude measure which does not distinguish between discretionary or automatic growth of revenue.

What is the elasticity of the tax system?

Overall tax elasticity was estimates to be about 1.03, suggesting that the responsiveness of the tax system to a unit change in GDP was more that unity thereby rejecting the hypothesis that the overall tax system is income inelastic in the long run. General and specific recommendations aimed at improving tax collection are made.

How is the responsiveness of the tax system measured?

This responsiveness is measured using two concepts – tax elasticity and buoyancy. While tax elasticity measures the response of revenue to income changes, net of discretionary tax measures, tax buoyancy measures the total response of tax revenue to changes in income.

Which is greater base to income or buoyancy?

Decomposition of the buoyancy coefficients into tax-to-base and base-to-income elasticities showed that the former was greater than the latter by their indices indicating that there is potential revenue in the economy which is untaxed.