What is minimum capital requirement for any life insurance company?

Insurers are required to have a minimum paid-up capital of ₹100 crore.

What are insurance capital requirements?

Specifically, the RBC instructions ascribe quantitative factors to each component of risk to which that insurer is subject — e.g., investment assets, liabilities, underwriting risk, credit risk, interest rate risk and others, yielding an amount of capital (“authorized control level”) that is deemed the minimum …

What is the requirement for the insurer under the risk based capital framework?

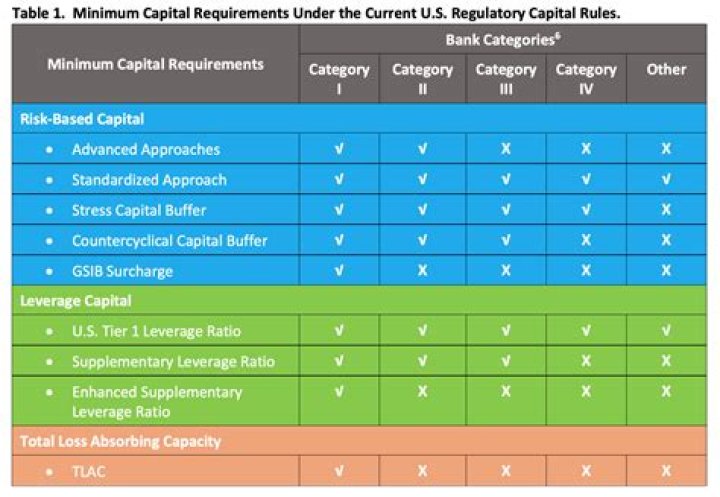

Risk-based capital requirements are minimum capital requirements for banks set by regulators. There is a permanent floor for these requirements—8% for total risk-based capital (tier 2) and 4% for tier 1 risk-based capital.

What is the capital base for life insurance?

Life insurers are expected to raise minimum paid-up capital from ₦2 billion to ₦8 billion; general underwriters from ₦3 billion to ₦10 billion; while composite and reinsurance companies have new minimum paid-up share capital requirements of ₦18 billion and ₦20 billion, up from ₦5 billion and ₦10 billion respectively.

Is it mandatory to maintain additional reserve for general insurance company?

The provision for reserve for Unexpired risks as given by solvency regulations take a cue from section 64V(1) (ii) (b) of the Insurance Act, 1938. In effect these two regulations stipulate the minimum reserve for unexpired risks and make it mandatory for every Non-Life Insurer to provide for such reserve.

Why do insurers hold capital?

Insurers hold capital to ensure that the promises made to policyholders will be met even under adverse conditions. The capital needed to fulfil this role must be calculated by reflecting the specific risk characteristics to which insurers are exposed.

How does risk based capital work?

Issue: Risk-Based Capital (RBC) is a method of measuring the minimum amount of capital appropriate for a reporting entity to support its overall business operations in consideration of its size and risk profile. It requires a company with a higher amount of risk to hold a higher amount of capital.

What is reinsurance coverage?

Reinsurance is insurance for insurance companies. It’s a way of transferring or “ceding” some of the financial risk insurance companies assume in insuring cars, homes and businesses to another insurance company, the reinsurer.

What are the different classes of insurance?

Broadly, there are 8 types of insurance, namely:

- Life Insurance.

- Motor insurance.

- Health insurance.

- Travel insurance.

- Property insurance.

- Mobile insurance.

- Cycle insurance.

- Bite-size insurance.

What is provision for unexpired risk?

Unexpired Risk Reserve is the present value of loss and expense payments to be provided for by premiums covering the period from the valuation date to expiry on all contracts in force on the valuation date. A loss reserve is a provision for an insurer’s liability for claims.

How do insurance companies raise capital?

An insurer raises capital which permits it to write an insurance policy. With its own capital plus the funds from insurance premiums, insurers must pay out claims from the insurance policies and the associated business expenses.

Under fixed capital standards, owners are required to supply the same minimum amount of capital, regardless of the financial condition of the company. The requirements required by the states ranged from $500,000 to $6 million and was dependent upon the state and the line of business that an insurance carrier wrote.

What are risk based capital requirements?

Risk-based capital requirement refers to a rule that establishes minimum regulatory capital for financial institutions. Risk-based capital requirements exist to protect financial firms, their investors, their clients, and the economy as a whole.

What are risk based capital requirements and what is their purpose?

RBC is one component used by regulators to conduct a financial analysis of insurance companies. The formula is used to derive a measure of “minimum capital” that an insurer would be expected to hold based on the types of risk to which the company is exposed.

How is Hlv calculated?

The HLV is calculated on the basis of three factors — age, current and future expenses, and current and future earnings. Let’s understand it with an example. Know your human life value here. This is a basic method of calculating your life insurance coverage needs and is based on your annual income.

How to calculate your life insurance needs, PWL capital?

Their regular monthly expenditures, not including daycare or the mortgage is $4,000 per month. They have a mortgage with a balance of $300,000, and pay $2,000 per month towards it. Part-time daycare is $1,000 per month. Retirement savings are $1,500 per month.

How many years of life insurance do you need?

The recommendation is to have seven to ten years of life insurance. It’s an easy method, but it doesn’t take into account the specific needs of survivors, other sources of funds — such as the survivors’ income and investments — or different types of family structures.

What are the minimum requirements for fixed capital?

How to calculate your clients life insurance needs?

The capital needs analysis is the most widely-used approach for estimating life insurance coverage. In addition to replacing the client’s salary, it also accounts for other sources of income and the specific needs of survivors. This method factors in: Current and future income of both the insured and surviving spouse