What is so special about recognizing revenues in governmental funds?

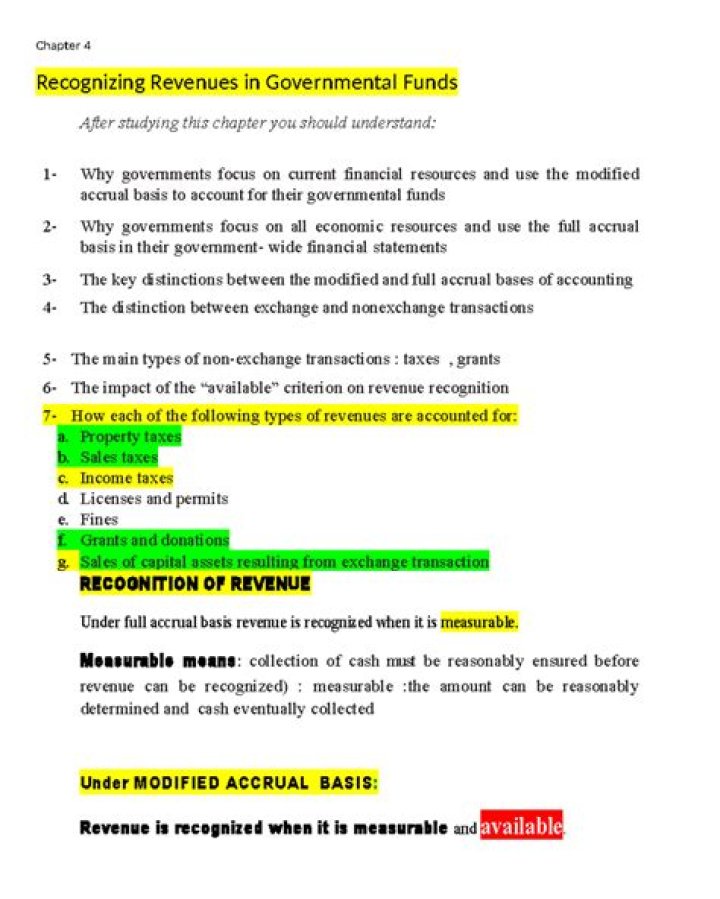

A governmental fund recognizes revenues (using the modified accrual basis of accounting) in the accounting period the revenues become both measurable and available to finance expenditures of the fiscal period.

How do governments determine whether a transaction is an exchange or non exchange transaction?

An exchange or exchange-like transaction is one in which each party receives and sacrifices something of approximate equal value. A non-exchange transaction is one in which one party receives something of value without directly giving value in exchange. Grants can be either exchange or non-exchange transactions.

What GASB 33?

33. Accounting and Financial Reporting for Nonexchange Transactions. (Issued 12/98) This Statement establishes accounting and financial reporting standards for nonexchange transactions involving financial or capital resources (for example, most taxes, grants, and private donations).

What is the purpose of Nonexchange revenue?

In a nonexchange transaction, a government gives (or receives) value without directly receiving (or giving) equal value in return. Nonexchange transactions are typically described as taxes, fines, and certain grants.

What revenue of general fund generally accrue?

Accrued revenue is revenue that has been earned by providing a good or service, but for which no cash has been received. Accrued revenues are recorded as receivables on the balance sheet to reflect the amount of money that customers owe the business for the goods or services they purchased.

What is derived tax revenue?

Derived tax revenues result from the taxes imposed by the State on exchange transactions. An exchange transaction resulting in derived tax revenues includes personal income taxes and certain consumption and use taxes and fees, business taxes, and other taxes.

What are the different types of revenue in exchange transactions?

Revenue from exchange transactions is derived from: (a) Sale of goods or provision of services to third parties; (b) Sale of goods or provision of services to other government agencies; and (c) The use by others of entity assets yielding interest, royalties and dividends.

What is the relationship between exchange and transaction?

The key difference between transaction and exchange is that a transaction is a contract or agreement between two parties where a good or service is exchanged in return for a monetary value whereas an exchange is a swap of a good or a service between two parties.

What Ipsas 23?

The objective of IPSAS 23 is to prescribe requirements for the financial reporting of revenue arising from non-exchange transactions, other than non-exchange transactions that give rise to an entity combination. In particular, these include revenue from taxes and transfers (both cash and non-cash transfers).

What is exchange revenue?

Groups gain exchange revenues when they receive funds for their goods and services of comparable value. Non-exchange revenues are funds that do not require an exchange of equal value.

What does general fund revenue mean?

General fund revenue means revenues from property taxes, licenses and permits, local taxes, service charges, and other types of revenue.

What is program revenue?

Program revenues are revenues that are directly attributable to a specific functional activity. Program revenues include fees collected from those who benefit from the program, grants, and other contributions required by the resource provider to support a specific activity.

What is the difference between exchange and transaction give example for both?

A transaction is the provision of goods and services in exchange for a set amount of money between two or more firms, parties and even accounts which results in the movement of value from one person to another. On the other hand, an exchange is the trade-off of services and goods between two parties.

What Ipsas 17?

The objective of IPSAS 17 is to prescribe the accounting treatment for property, plant and equipment so that users of financial statements can discern information about an entity’s investment in its property, plant and equipment and any changes in such investment.