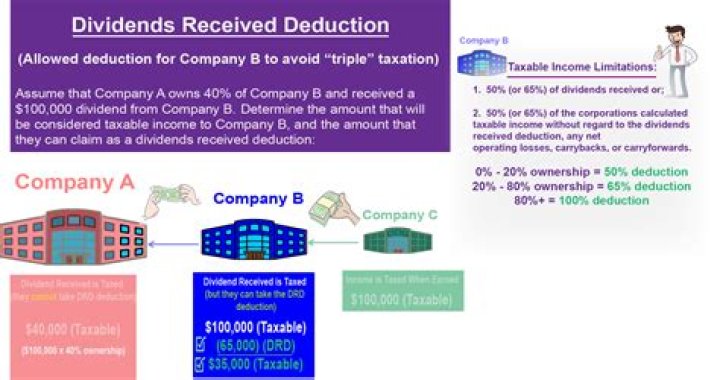

What is the purpose of the dividends received deduction DRD for corporations receiving dividends from another corporation What are the DRD percentages?

* Assumes a 35% tax rate for the corporation receiving the dividend. The DRD is designed to soften the blow of triple taxation on corporate dividends. Triple taxation occurs because the company paying the dividend does so with after-tax money.

How do you qualify for dividends received deduction?

In order to receive the tax benefit of a dividends received deduction, a corporate shareholder must hold all shares of the distributing corporation’s stock for a period of more than 45 days.

Is dividend received deduction a permanent difference?

Essentially, a percentage of dividends received by that corporation are deductible (not included) for calculating taxable income. Dividends received deductions are not considered as expense items for calculating net income. This will always result in a permanent tax difference.

Why does Congress provide the dividends received deduction for corporations receiving dividends?

Why does Congress provide the dividends received deduction for corporations receiving dividends? The percentage is determined based on the actual ownership of the receiving corporation in the distributing corporation’s stock. If the ownership is less than 20%, the dividends received deduction percentage is 70%.

How are dividends received by a company taxed?

Dividends There typically is no withholding tax on dividends paid by UK companies under domestic law, although a 20% withholding tax generally applies to distributions paid by a REIT from its tax-exempt rental profits (subject to relief under a tax treaty).

Is dividend paid deductible?

First, the dividends distributed by the corporation are profits (part of the business net income) not business expenses and are not deductible. So the corporation pays corporate income tax on profits distributed to shareholders. Then, the shareholders pay income taxes personally on those dividends.