What type of return is 1041?

U.S. Income Tax Return for Estates and Trusts

IRS Form 1041, U.S. Income Tax Return for Estates and Trusts, is required if the estate generates more than $600 in annual gross income. The decedent and their estate are separate taxable entities. Before filing Form 1041, you will need to obtain a tax ID number for the estate.

How are inter vivos trusts taxed?

Benefit #1 – Marginal Tax Rates for the Testamentary Trust Under s99A, an Inter Vivos Trust will be assessed at the highest marginal tax rate for undistributed income, that is, at 49% inclusive of Medicare and Budget Levies.

Is inter vivos the same as living trust?

An Inter Vivos Trust is one created by a living person for the benefit of another person. Also known as a living trust, this trust has a duration that is determined at the trust’s creation and can entail the distribution of assets to the beneficiary during or after the trustor’s lifetime.

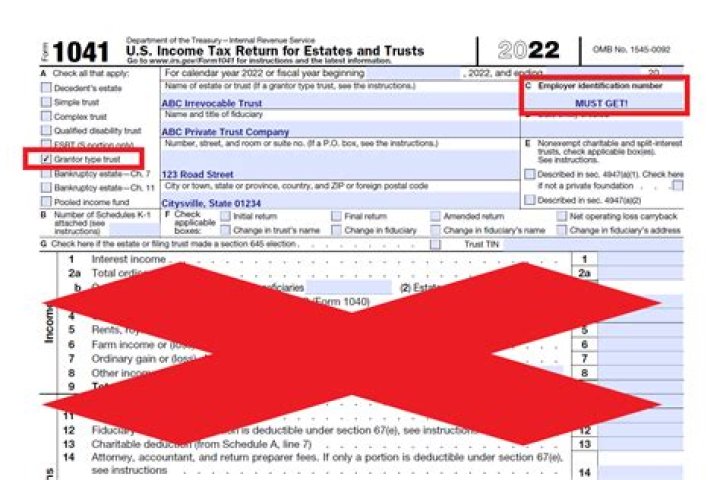

What do you need to know about 1041 tax return?

About Form 1041, U.S. Income Tax Return for Estates and Trusts. The fiduciary of a domestic decedent’s estate, trust, or bankruptcy estate files Form 1041 to report: The income, deductions, gains, losses, etc. of the estate or trust.

What is the difference between a 1041, 1040A and 1040EZ?

The Internal Revenue Service provides three options for personal income tax filing: Form 1040EZ, 1040A and 1040. Form 1041 is the income tax return for estates and trusts. While you’ll be required to file form 1041 if you are filing for a trust, what form you choose for your personal taxes will…

How does an estate or trust file a 1041?

An estate or trust is treated as its own entity as far as taxes are concerned. The 1041 includes all income and deductions that are allowed per the IRS guidelines. However any distributions that are made to beneficiaries of the estate or trust are filed on a schedule K-1.

Can a 1041 be filed on a schedule K?

The 1041 includes all income and deductions that are allowed per the IRS guidelines. However any distributions that are made to beneficiaries of the estate or trust are filed on a schedule K-1. The estate or trust does not pay taxes on the distributions to beneficiaries.