When you apply for refinance a mortgage What happens?

Refinancing a mortgage involves taking out a new loan to pay off your original mortgage loan. In many cases, homeowners refinance to take advantage of lower market interest rates, cash out a portion of their equity, or to reduce their monthly payment with a longer repayment term.

How long does it take for a refinance to be approved?

A refinance typically takes 30 – 45 days to complete. However, no one will be able to tell you exactly how long yours will take. Appraisals, inspections and other third parties can delay the process. Your refinance might be longer or shorter, depending on the size of your property and how complicated your finances are.

What steps are involved in refinancing a loan?

The Refinance Process – What to Expect

- Step One: Check Your Credit.

- Step Two: Compare Types of Loans.

- Step Three: Gather Documents.

- Step Four: Apply for a Loan.

- Step Five: Get an Appraisal.

- Step Six: Go Through Underwriting.

- Step Seven: Lock in Your Rate.

- Step Eight: Close Your Loan.

When is it a good time to refinance your mortgage?

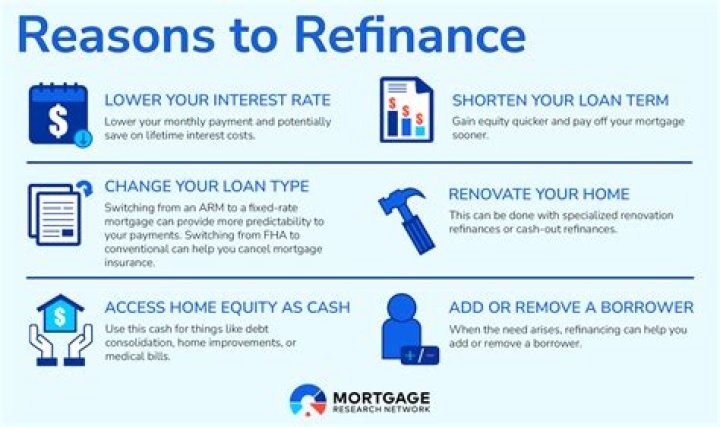

Getting a mortgage with a lower interest rate is one of the best reasons to refinance. When interest rates drop, consider refinancing to shorten the term of your mortgage and pay significantly less in interest payments.

Why is it a good idea to refinance your home?

These homeowners may justify the refinancing by the fact that remodeling adds value to the home or that the interest rate on the mortgage loan is less than the rate on money borrowed from another source. Another justification is that the interest on mortgages is tax deductible.

What happens to your interest rate when you refinance your mortgage?

Reducing your interest rate not only helps you save money, but it also increases the rate at which you build equity in your home, and it can decrease the size of your monthly payment. For example, a 30-year fixed-rate mortgage with an interest rate of 5.5% on a $100,000 home has a principal and interest payment of $568.

What should I look for when refinancing my mortgage?

When you apply to refinance, your lender asks for the same information you gave them when you bought the home. They’ll look at your income, assets, debt and credit score to determine whether you can pay back the loan. Your lender will also need your spouse’s documents if you’re married.