Which of the following taxpayers Cannot use the cash method of accounting?

The following taxpayers are not prohibited from using the cash method of reporting: Any corporation or partnership that has an average annual gross receipt of $25 million or less for the 3 preceding tax years.

Which of the following criteria is not required for a meal to be considered a tax deductible business meal quizlet?

The term _ is used to describe an expense that is helpful or conducive to a business activity. Which of the following criteria is NOT required for a meal to be considered a tax-deductible business meal? The meal must be eaten on the business premises.

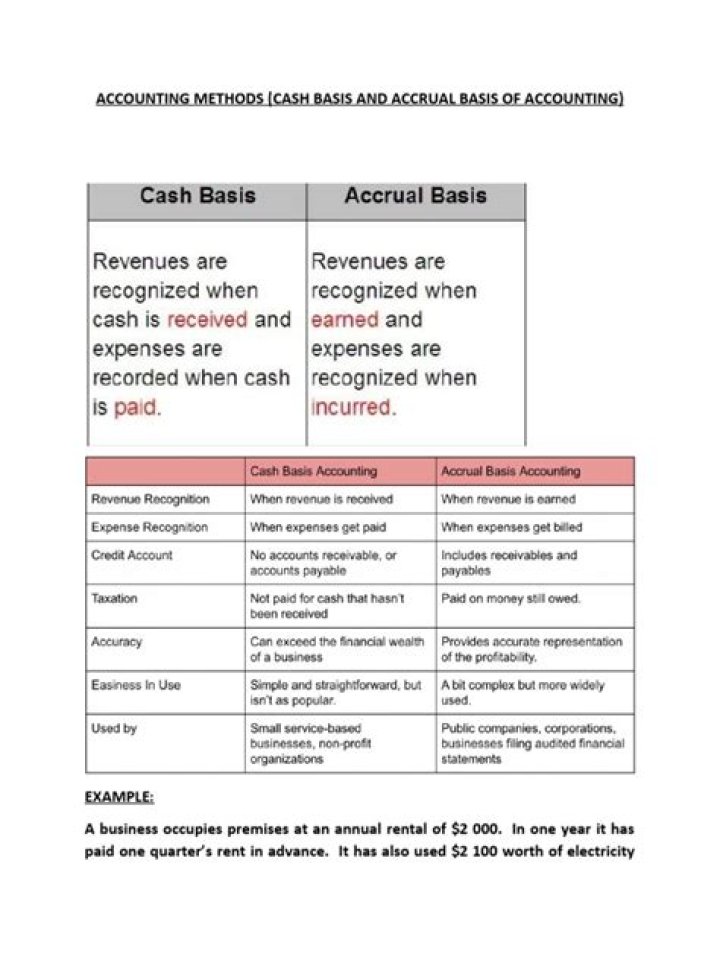

What are the different accounting methods allowed for tax purposes?

The most commonly used accounting methods are the cash method and the accrual method. Under the cash method, you generally report income in the tax year you receive it, and deduct expenses in the tax year in which you pay the expenses.

Which of the following would be considered constructive receipt of income?

Constructive receipt refers to situations where income can be used despite the fact that this money has not yet been physically received. Taxpayers must include any income on their taxes based on the year that income was constructively received, even if they don’t have possession of the funds.

What type of business can be designated as profit or non profit?

Corporations can be designated either as profit or nonprofit.

What makes a not for-profit organization?

A nonprofit organization is one that qualifies for tax-exempt status by the IRS because its mission and purpose are to further a social cause and provide a public benefit. Nonprofit organizations include hospitals, universities, national charities and foundations.

When is tax cannot follow accounting PwC?

When recognized by the taxpayer, only the income tax effect (or the 30% thereof) of the resulting NOLCO is recorded as a debit to the DTA and as a credit to income tax expense. DTA is an account presented in the balance sheet while income tax expense is reflected in the income statement but not as a regular expense.

When is tax is too rigid to follow accounting?

However, over the years, I have come across some tax rules which are too rigid or impractical to follow, and at times are even inconsistent with the objectives the government is trying to achieve.

Which is an example of tax cannot follow accounting?

An example is RR No. 21-2002, which details the additional procedural and documentary requirements for the preparation and submission of financial statements (FS) that accompany the tax returns under Section 6 (H) of the Tax Code.

Is it appropriate to deduct NOLCO as a special deduction?

With all due respect, I believe that it is not appropriate to require the presentation of NOLCO as a special deduction in the audited FS because it is inconsistent with Philippine Accounting Standards (PAS).